Some investors use bond ladders for fixed income exposure. A portfolio of bonds with maturities spaced out across a range of years provides a stream of cash flows that decreases the uncertainty around meeting future liabilities. But the tradeoff for this benefit is potentially leaving returns on the table.

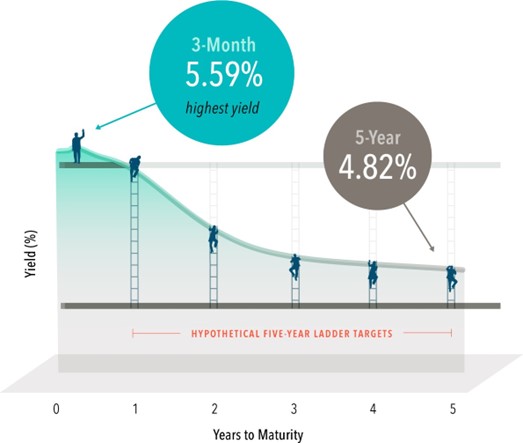

Take a five-year Treasury ladder, for example. This approach provides exposure across the zero-to-five-year segment of the yield curve. As of October 31, 2023, the highest yield within Treasuries could be found at three months. But the ladder buys throughout the available maturities, which offer increasingly lower yields. Bond ladders ignore information in prices about expected returns.

Laddering also exposes investors to the typical drawbacks of purchasing individual bonds. A lack of diversification constrains the opportunity set, preventing investors from increasing expected returns through credit exposure or enjoying economies of scale in transaction costs.

Bond ladders are a tradeoff that comes with risk, just like step ladders—and there’s a reason I don’t do my own roof repairs.

Exhibit 1: Slippery Slope

US Treasury yields, October 31, 2023

Past performance is not a guarantee of future results.

Source: Department of the Treasury.

DISCLOSURES

The information in this document is provided in good faith without any warranty and is intended for the recipient’s background information only. “Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. Please click here to read the full text of the Dimensional Fund Advisor Disclaimer.