- You are here:

- Home »

- Blog »

- Financial Education & News »

- Market Review 2021: A Recovery Amid Challenges

Market Review 2021: A Recovery Amid Challenges

It was a year of uncertainty and anticipation, of hopes for a return to a degree of normalcy following the onset of the COVID-19 pandemic in 2020. And it was a year that showed, again, the difficulty of making investment decisions based on predictions of where markets will go—as well as the enduring benefits of diversification and flexibility.

Coming out of a volatile 2020, investors sought signals as to which way the global economy was headed. The distribution of vaccines and the easing of lockdowns were followed by an economic rebound, but the emergence of new variants would be a setback for the recovery. Despite these challenges, global gross domestic product grew, completing the transition from recovery to expansion and eventually surpassing its pre-pandemic peak.

Still, the recovery would be accompanied by labor shortages, supply chain issues, and rising inflation. Prices increased especially rapidly in areas such as food and energy, and the US consumer price index jumped 6.81% from year-earlier levels in November, a rise unseen in nearly four decades. The media was filled with debates about where inflation would go, what was causing it, how long it might last, and what could, or should, be done in response. (An investor pondering those questions might take comfort knowing that many assets in the past have outpaced even above-average inflation.)

Throughout the year, the market continued a relatively steady rise, with large cap stocks in the US ending 2021 near a record high. The S&P 500 Index1 generated returns of 28.71%. In addition to the effective vaccines, markets were buoyed by a number of other positive developments, including strong corporate earnings and increased consumer demand. In the third quarter, US corporations pulled in record profits—both in dollar terms and as a share of GDP (11%).2 That came as consumer spending generally trended higher throughout the year, rebounding from pandemic lows.

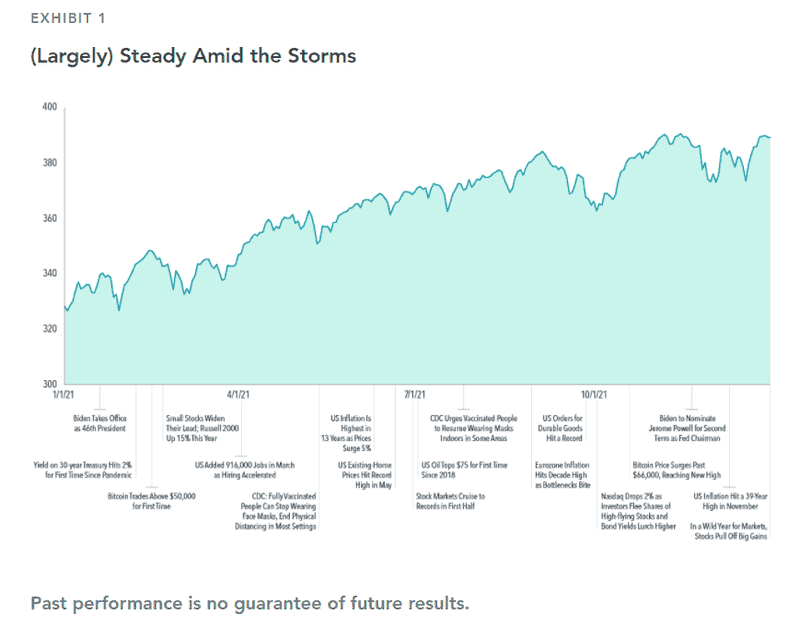

Likewise, global markets continued to rise alongside those in the US, despite some setbacks, as Exhibit 1 shows. Markets that started the year strong were up and down in the year’s second half but still near all-time highs. Global equities, as measured by the MSCI All Country World Index,3 increased 18.54%. Developed international stocks, as represented by the MSCI World ex USA Index, rose 12.62%, notably stronger than emerging markets, which saw the MSCI Emerging Markets Index fall –2.54%.

Value stocks, or those with lower relative prices, began the year strong as the economy reopened and interest rates were rising. But growth stocks rallied later in the year. That shift came as the Delta variant and the resurgent pandemic brought back concerns that dominated in the first half of 2020. Over the long term, value stocks have generally outperformed growth stocks—by 2.66% based on average annualized returns since July 1926 in the US—but premiums are subject to disappointing periods. Still, data covering nearly a century backs up the notion that value stocks have higher expected returns. And value premiums have often shown up quickly and in large magnitudes, as they did in late 2020 and early 2021.

Fixed income markets experienced more tepid returns than the equity markets, with the Bloomberg Global Aggregate Bond Index returning –1.39%. After widening in 2020, credit spreads ended 2021 at levels narrower than pre-pandemic levels. For the year, corporate bonds generally outperformed their government counterparts. The dispersion between the two asset classes was much less pronounced than during the previous year, with global corporate bonds outperforming global Treasury and government-related bonds by 0.82%.4

However, return deviations were still pronounced between inflation-protected and nominal bonds, as realized inflation was higher than expected inflation. The five-year break-even inflation rate increased from 1.95% to as high as 3.17% late in the year, before ending the period at 2.87%.5 For the year, nominal US Treasuries returned –2.32%, while US Treasury Inflation Protected Securities (TIPS) returned 5.96%.6

Global yield curves finished the year generally higher and steeper than at the start. US Treasury yields, for example, rose across the board, with larger increases along the intermediate portions of the curve. Longer-dated bonds generally underperformed short-term bonds, with intermediate-term US Treasuries returning –1.72% and short-term US Treasuries returning 0.04%.7

A Focus on Inflation and Debt

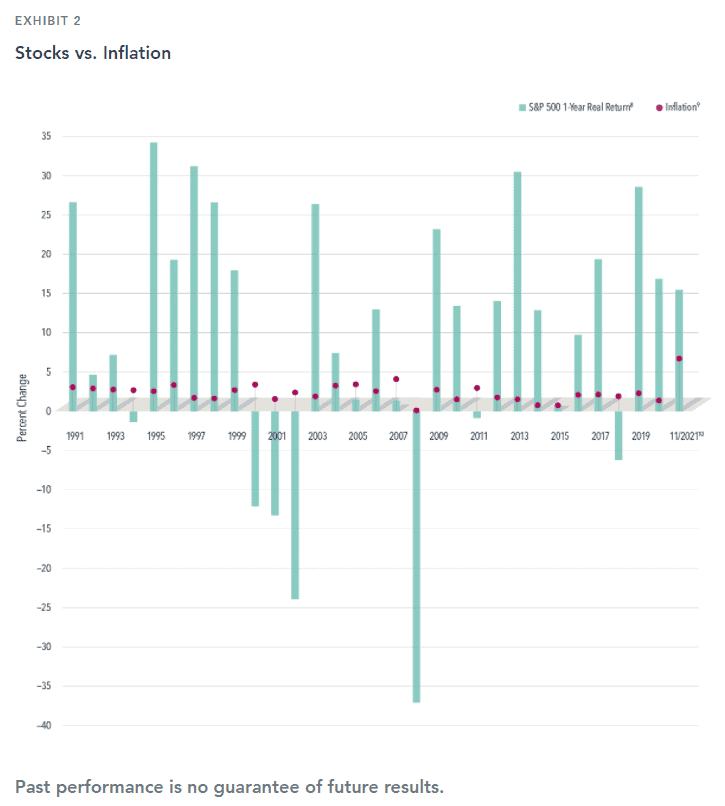

For investors worried about the impact of inflation on their portfolios, it is important to remember that US stocks since 1991 have generally provided returns that outpaced inflation. This is a valuable reminder for those concerned that today’s rising prices will make it harder to reach long-term financial goals. As seen in Exhibit 2, equity performance in the past three decades does not show any reliable connection between periods of high (or low) inflation and US large cap stock returns. The weakest returns can occur when inflation is low, and 23 of the past 30 full years saw positive returns even after adjusting for the impact of inflation.

Like in equities, when it comes to fixed income there is no reason to assume inflation will bring dire effects. From 1927 through 2020, median inflation was 2.68%, and in the 47 years when inflation exceeded that rate, it averaged 5.49%. Many types of bonds beat inflation over those 47 years, which included double-digit inflation in the 1940s and 1970s. For investors particularly sensitive to the potential for rising prices, inflation-hedging assets such as TIPS can help protect investors, as can strategies that focus on real (inflation-adjusted) returns. Bond investments should always be matched to an investor’s goals—they aren’t one-size-fits-all. But inflation concerns needn’t scare one away from fixed income.

Rising government debt levels may also lead some investors to worry about an adverse impact on stock returns. The US debt held by the public topped $22 trillion,11 up more than $5 trillion from the end of 2019 and 123% of GDP. In a more extreme example, China’s overall debt was 263% of its GDP late in 2021, driven by massive government sponsored infrastructure and property investment, as evidenced by China’s beleaguered Evergrande Group, which defaulted on its debt in December. However, the relation between country debt and stock markets is complex, in part because sovereign solvency is dependent upon many factors besides just debt levels. In addition, debt is generally a slow-moving variable whose expected value should be incorporated in market prices. Consistent with this belief, the evidence suggests there has not been a strong relation between country debt and equity market returns.

Remaining Flexible in a Fast-Moving Market

Spiking inflation and the ups and downs tied to the COVID-19 pandemic weren’t the only types of volatility drawing attention in 2021. Bitcoin and many other cryptocurrencies continued rising, prompting many investors to wonder whether this new form of electronic money deserves a place in their portfolios. But in its relatively short existence, bitcoin has proved prone to extraordinary swings, sometimes gaining or losing more than 40% in price in a month or two. Any asset subject to such sharp volatility may be catnip for traders but of limited value as a reliable medium of exchange (to replace cash), as a risk-reducing or inflation-hedging asset (to replace bonds), or as a replacement for other assets in a diversified portfolio. Thus, while cryptocurrencies may hold some appeal for adventurous investors, it’s hard to make a case for a significant allocation of one’s overall assets to them in the current moment.

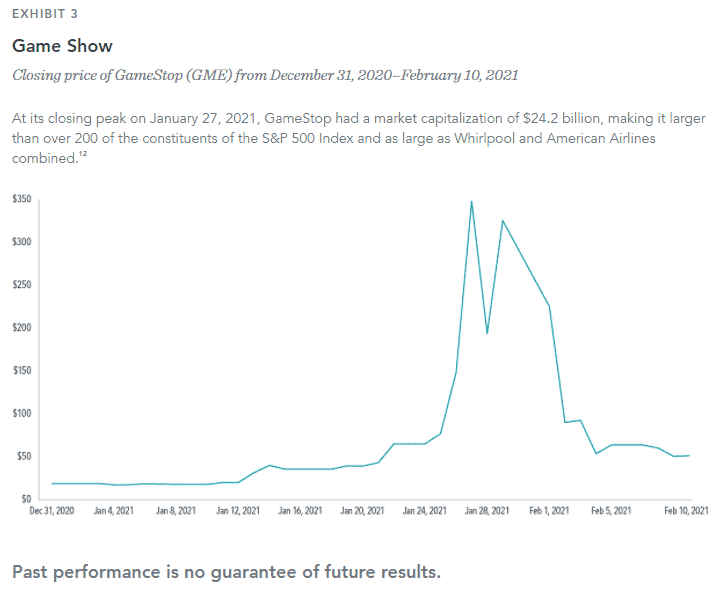

Another market curiosity arose in early 2021, when individual investors and others helped bid up shares of videogame retailer GameStop, as Exhibit 3 shows. GameStop shares and other so-called “meme stocks” benefited from these investors’ enthusiasm. But as the price of GameStop climbed, along with its market cap, the small cap value stock quickly stopped being either.

The case of GameStop highlights the importance of having a systematic process in place to respond to new information about securities and their expected returns on a daily basis. In contrast, an index-tracking approach does not have the same flexibility to respond to price changes; by design, an index will wait to respond until its next periodic reconstitution date—potentially resulting in style drift. Some small cap indices holding GameStop quickly saw it become the largest index holding as the stock price increased, and those indices generally continued to hold it as the price fell. Daily portfolio management can spare investors from such style drift by rebalancing portfolios incrementally over time, keeping them focused on the targeted asset allocation and putting investors in a better position to capture higher returns.

Concentrating your portfolio in a few hot stocks or cryptocurrencies—like focusing on any small number of holdings—can expose investors to substantial risk. Even if you manage to find a few winners, research argues that good luck is unlikely to repeat throughout a lifetime of investing. For every individual who got into and out of a hot stock or cryptocurrency at the right time, there’s likely another who bought or sold at the wrong time.

When Breaking Records Sounds Like a Broken Record

In a similar way, there may be a tendency to think markets reaching a new high is a signal stocks are overvalued or have approached a ceiling. Such concerns may be especially potent now, with the S&P 500 having notched 75 closing records in 2021 on a total-return basis. However, investors may be surprised to find that the average returns one, three, and five years after a new month-end market high are similar to the average returns over any one-, three-, or five-year period. For instance, in looking at monthly returns between 1926 and 2021 for the S&P 500 Index, 30% of the monthly observations were new highs. After those highs, the average annualized compound returns ranged from over 14% one year later to more than 10% over the next five years. Those results were close to the average returns over any given period of the same length. Put another way, reaching a new high doesn’t mean the market will retreat. Stocks, at any time, are priced to deliver a positive expected return for investors, so reaching record highs regularly is the outcome one would expect.

This is a good reminder of the power of markets. Investors can’t predict the nature or timing of the next crisis, or the end of any existing ones. But markets are forward-looking and reflect optimism. New challenges will await, but rather than guessing at what will happen, investors can choose to trust markets and their long-term prospects. The year 2021 was one that emphasized the benefits of discipline and diversification, of planning and perseverance, in a market that was uncertain (like markets in all the years before it). As we enter 2022, looking backward can help as investors look to the future.

FOOTNOTES

- S&P data © 2022 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Indices are not available for direct investment.

- Data is based on after-tax corporate profits from current production and is according to estimates from the US Bureau of Economic Analysis.

- MSCI data © MSCI 2022, all rights reserved. Indices are not available for direct investment.

- Global corporate bonds represented by the Bloomberg Global Aggregate Corporate Index. Global Treasuries represented by the Bloomberg Global Aggregate Treasuries Index. Government-related bonds represented by respective Bloomberg government-related indices. Data provided by Bloomberg. Indices are not available for direct investment.

- Five-year break-even inflation rate data from Federal Reserve Bank of St. Louis as of December 31, 2021.

- US Treasuries represented by the Bloomberg US Treasury Bond Index. US TIPS represented by Bloomberg US Treasury Inflation-Linked Bond Index. Data provided by Bloomberg. Indices are not available for direct investment.

- Intermediate-term US Treasuries represented by Bloomberg US Intermediate Treasury Index and short-term US Treasuries represented by Bloomberg US Short Treasury Index. Data provided by Bloomberg. Indices are not available for direct investment.

- Real returns illustrate the effect of inflation on an investment return and are calculated using the following method: [(1 + nominal return of index over time period) / (1 + inflation rate)] − 1. S&P data © 2022 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

- Based on non-seasonally adjusted 12-month percentage change in Consumer Price Index for All Urban Consumers (CPI-U). Source: US Bureau of Labor Statistics.

- Year-to-date data for 2021 through November 30.

- As of September 30, 2021, according to the US Treasury Department.

- Source: S&P and Dow Jones data © 2022 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

GLOSSARY

Nominal return: The rate of return on an investment without adjusting for inflation.

Value premium: The return difference between stocks with low relative prices (value) and stocks with high relative prices (growth).

DISCLOSURES

The information in this blog is provided in good faith without any warranty and is intended for the recipient’s background information only. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision.

About the Author Doug Finley

Douglas Finley, MS, CFP, AEP, CDFA founded Finley Wealth Advisors in February of 2006, as a Fiduciary Fee-Only Registered Investment Advisor, with the goal of creating a firm that eliminated the conflicts of interest inherent in the financial planner – advisor/client relationship. The firm specializes in wealth management for the middle-class millionaire.

Related Posts

The Power of the Market, the Ultimate AI

The Cost of Trying to Time the Market

Market Behavior and the Weather

Curve Your Enthusiasm with Fed Activity

Bringing Order to Your Investment Universe Part 2: Transitions and Taxes

Bringing Order to Your Investment Universe Part 1: The Beauty of Being Organized

Protecting Women’s Wealth

What I See When I Watch Basketball

Session expired

Please log in again. The login page will open in a new tab. After logging in you can close it and return to this page.